Archive: April 2017

Champagne and Burgundy Continue to Surge

The Champagne category performed well in the first quarter of 2017, as indicated by prices for 1996 Krug Clos de Mesnil, +43.8% over 8 trades in the first quarter. Prices for the regular 1996 Krug Brut and the 1990 Dom Perignon were up more modestly at +7.3% and +11.1% on a broader base.

Top Bordeaux wines were flat or down moderately in the period: ’89 Haut-Brion was -0.9%, ’82 Lafite was +1.3% and 1990 Cheval was +3.8%, while 2000 Petrus was -9.2% and ’89 Lynch Bages was -13.9%

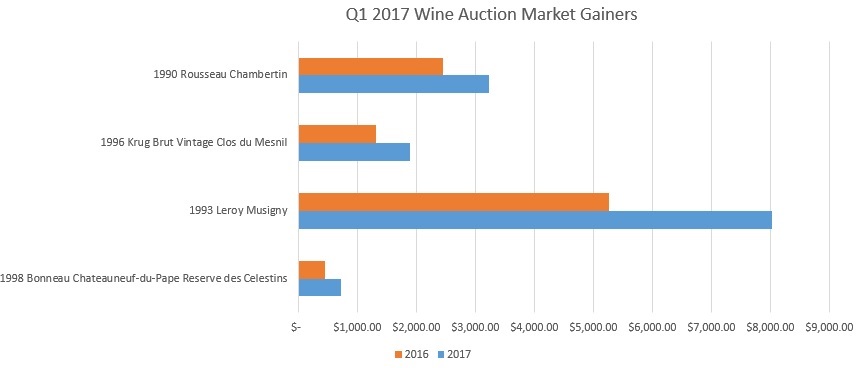

Growth continued for many Burgundy wines. The biggest gainer was ’93 Leroy Musigny at +52.5%, but there was only one trade during the period (in the Acker Grunewald sale), although other vintages of the same wine also showed sharp growth and Leroy generally has been very buoyant in spite of fairly high prices. 1990 Rousseau Chambertin continued to show good growth at +31.9%, and even younger vintages, such as the 2010 Liger-Belair La Romanee was +9.4%. Some of the less well-known wines showed slower growth however: no ’09 Cathiard Malconsorts came to market, but the ’05 vintage was +3.7% in the period, and the ’05 Fourrier Clos Saint-Jacques was +0.9%.

Results were mixed for white Burgundy. 1996 Coche Corton Charlemagne showed comparatively modest growth at +2.9%, but 2005 DRC Montrachet was +57.5% over 11 bottles trading hands, with 9 of them at Acker’s Chinese New Year sale.

Elsewhere, prices were generally higher for Rhone wines. ’90 Rayas was +14.5%, and ’98 Bonneau Celestins showed the most growth of any indicator in the period at +62.8%. Others, however, had dropped: ’78 La Chapelle was -1.4% (no ’61 traded hands), and the ’99 La Mouline was -17.7% with 50 bottles trading hands. Italian wine drooped slightly: ’07 Masseto was -6.5% in spite of a strong showing at the Sotheby’s New York sale, and ’90 Monfortino was -4.9%.

New World wines were mixed. ’01 Grange was +4.3%, but ’97 Screaming Eagle was -3.8%, and ’94 Dominus was -5.7%, while Port continued to show modest growth, with ’63 Nacional +7.6% and ’77 Taylor’s at +4.0%.

Wine auction market sales sharply higher

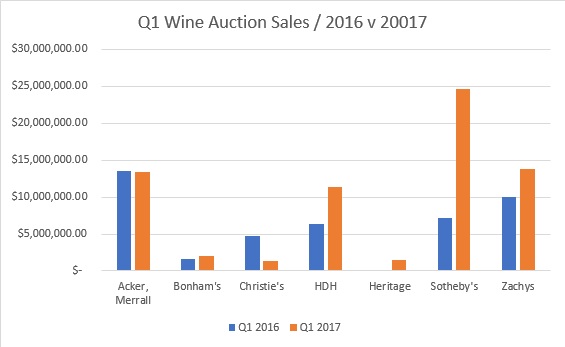

The wine auction market showed ruddy good health in the first quarter of 2017 after a somewhat slow initial start. Total volume through the marketplace was $68.1 million, as compared to $43.5 million during the same period last year. The average lot value this year is considerably higher, at $3,938 this year as compared to $3,168 last year, and the total number of lots coming to sale is also up – from 15,001 in Q1 last year to 19,111 this year, with three more sales on the calendar. In addition, the average sell-through rate was more robust, with 92.52% of lots offered finding buyers as compared to 91.75% last year.

Sotheby’s continued to lead the market, with a total of $24.6 million in the quarter over seven sales, with an average sell-through rate of 93.8%. This total included a three-sale set of single owner sales all from the same anonymous vendor that totaled $9.3 million. While not the magnitude of last year’s Koch sale, this was still a significant sale, and their success with big single owner sales continues to help business getting on this front. They have recently announced the sale of another tranche from the Don Stott collection for May 20th, with a presale estimate of $2m – $2.8m.

Second place was won by Zachys at $13.8 million, driven in part by their very successful La Paulée auction, worth $7.9 million. The average sell through rate of 98.3% outperformed the marketplace. This is a very strong result, particularly given the fact that there was only one sale in Hong Kong and one sale in New York during the quarter. Zachys just edged out Acker, Merrall, who sold $13.5 million over four sales, while HDH sold $11.3 million in the quarter with their two Chicago sales, selling every one of their lots for what some would call a “white glove” result.

Christie’s and Bonhams were both slower than last year, albeit off a smaller base. Dallas-based Heritage organized a sale in Beverly Hills, while last year they did not during the first quarter.

Neapolitan Treasures

Delicious, elusive, compelling, frustrating, the wines of Campania have long been among my favorites. This ancient region has been producing marvelous wine since before the foundation of Rome, and there are wines from this region that rank among the best produced in all of Italy. They are less well-known abroad, perhaps, since they are produced from indigenous varieties. Some of these, such as Fiano and Greco among the whites, and Aglianico among the reds are becoming more well-known. Savvy wine lovers, however, will want to explore the full range, as they offer thrilling tastes and flavors, and often provide extraordinary value for money.

This being said, such a quest is often complicated by limited availability. Having tasted several hundred wines from Campania last week, I was frustrated by the limited availability of the top wines. Although this is undeniably true (and perhaps understandable), there were a number of interesting wines that are available – at least online, if not at your local store. I rated a number of the wines last week as either very good (***) or outstanding (****). Here are a few notes on those one might find: